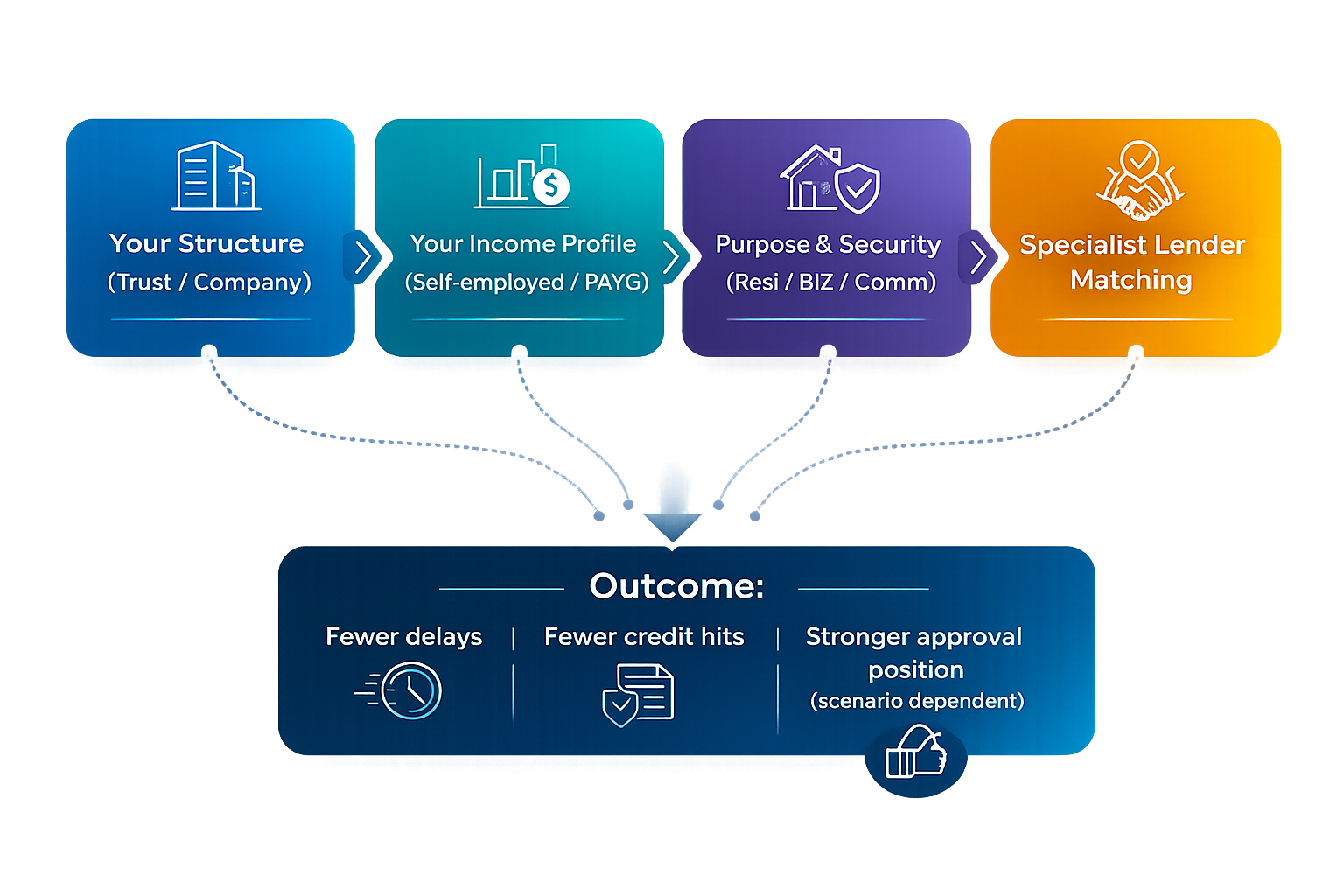

Trust and company structures are not assessed the same way by every lender. Some lenders understand complex structures and self‑employed income well, while others apply a strict “one‑size‑fits‑all” policy, which can lead to unnecessary delays or declines.

As trust and business lending specialists, we maintain relationships with lenders suited to different trust and business scenarios. Our role is to match your structure, income profile, and lending purpose to the lender most likely to support it before an application is submitted.

This approach reduces delays, avoids unnecessary credit enquiries, and gives you the best chance of approval with the right lender the first time.