Importantly, no major new tax changes were announced for superannuation in this Budget.

However, several previously legislated changes commence on 1 July 2026, including the new Division 296 tax and Payday Super.

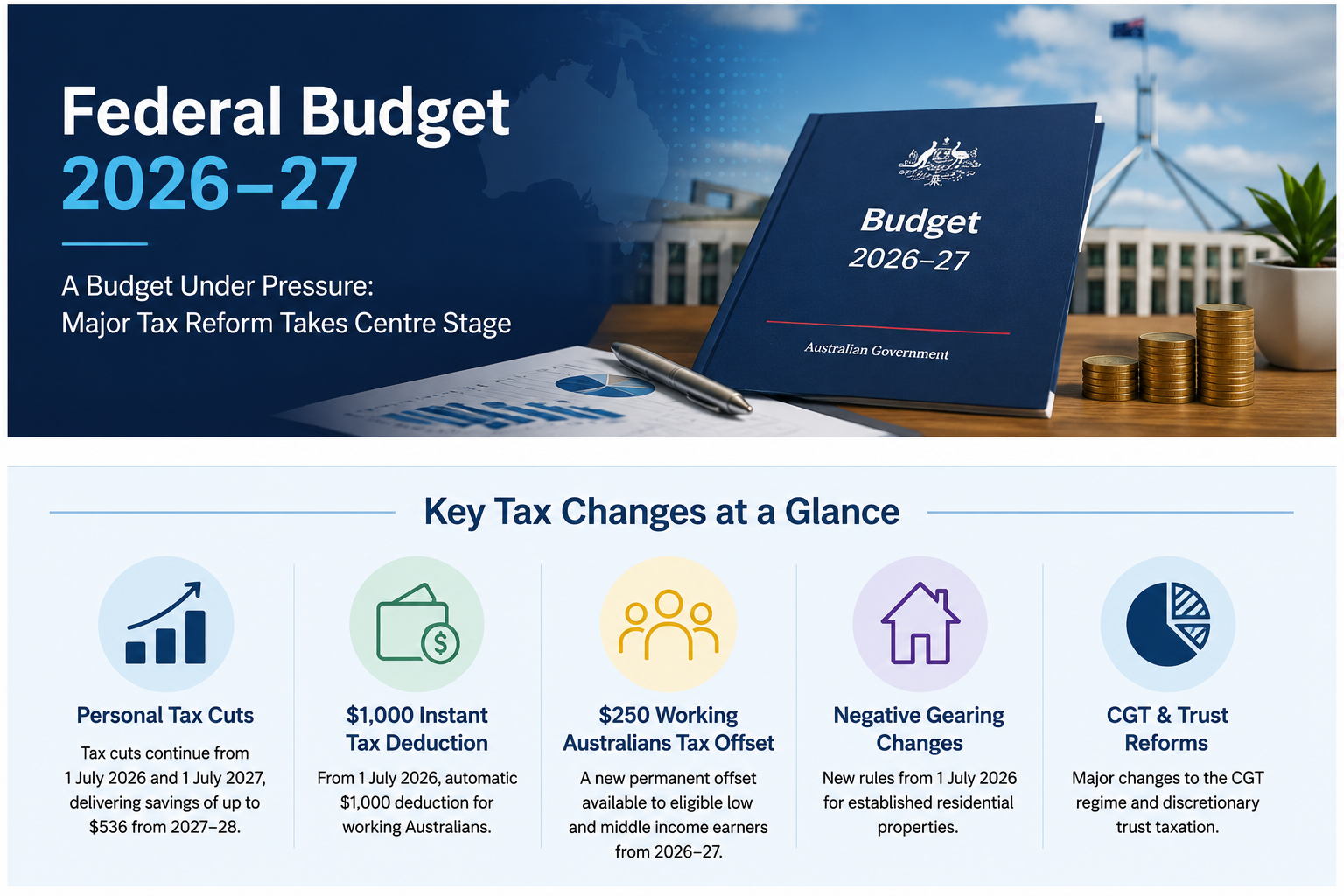

On 12 May 2026, Treasurer Jim Chalmers delivered the 2026-27 Federal Budget — described in the Budget speech as “the most important and ambitious Budget in decades.” Delivered against an uncertain global backdrop, including the ongoing Middle East conflict and persistent cost-of-living pressures, the Budget pairs sustained spending on health, housing, defence and resilience with the most significant package of personal and investment tax reforms in a generation.

A word of caution before acting

As we have advised clients before, it is important not to make decisions yet — these are government policy announcements. Given the Opposition Reply to the Budget, the current commentary and a great deal of conjecture around these announcements, it is unlikely that all of the measures will be passed in their current form. There is a likelihood that some of these will be passed, although, as has happened in the past, those measures could subsequently be unwound in the event that the current Labor Government is not returned to power.

It should also be noted that the attack on negative gearing was first commenced by the former Labor Treasurer Paul Keating in 1985-86, and was unwound two years later when Labor went to the polls — they were going to lose the election if it had remained. Likewise, the original introduction of the capital gains tax, which applied from 20 September 1985, was severely changed. It is unfortunate that the current Treasurer appears adamant to continue making the same mistakes of his mentor, Paul Keating, and that he wants to force Australia into having a “recession we have to have” — as Paul Keating famously stated in the late 1980s and early 1990s, which led to the recession of 1991.

The headline story is tax reform. The Government has announced sweeping changes to the capital gains tax (CGT) regime, negative gearing on established residential properties, and the taxation of discretionary trusts — alongside continued personal income tax cuts, a new $250 Working Australians Tax Offset, and a $1,000 instant tax deduction. For businesses, the $20,000 instant asset write-off becomes permanent, the loss carry-back rules return, and the R&D Tax Incentive is being recalibrated.

The Budget delivers an underlying cash deficit of $31.5 billion for 2026-27, forecast to widen slightly to $34.4 billion before improving to a deficit of $25.3 billion by 2029-30. Compared to the December MYEFO, the budget position over the forward estimates has improved by $44.9 billion.

At a glance

The five priorities of Budget 2026-27

- Cost-of-living relief — extended energy and fuel support, cheaper medicines, expanded urgent care clinics.

- Fuel supply and security — a $14.8 billion fuel resilience package and a domestic gas reservation from 1 July 2027.

- Productivity and resilience — R&D, AI adoption, skills, regulatory streamlining and supply-chain investment.

- Tax reform — CGT, negative gearing, discretionary trusts and personal tax overhaul.

Housing and infrastructure — $5.9 billion extra for the Help to Buy scheme, $2 billion for housing-enabling infrastructure and major rail projects.

Spending highlights

Headline spending commitments in the Budget include:

reaching 3% of GDP by 2033

grants, science, defence and research

under the National Health Reform Agreement

Australia's energy supply

Pharmaceutical Benefits Scheme

Home Buyers (Help to Buy) program

5,000 additional beds per year

zero the heavy-vehicle road user

charge for three months from 1 April 2026

including frontline staff and myGov upgrades

and supply of new homes

Clinics permanent

reaching 3% of GDP by 2033

grants, science, defence and research

under the National Health Reform Agreement

Australia's energy supply

Pharmaceutical Benefits Scheme

Home Buyers (Help to Buy) program

5,000 additional beds per year

zero the heavy-vehicle road user

charge for three months from 1 April 2026

including frontline staff and myGov upgrades

and supply of new homes

Clinics permanent

All figures are estimates. Source: Commonwealth of Australia, Budget Paper No. 2, 2026-27.

Personal taxation

Legislated tax cuts continue

The legislated personal income tax cuts continue to roll through. From 1 July 2026, the 16% marginal rate applying to income between $18,201 and $45,000 reduces to 15%. From 1 July 2027, it will be further reduced to 14%.

These cuts deliver tax savings of up to $268 in 2026-27 and up to $536 from 2027-28, compared with current settings.

| Thresholds ($) | 2024-25 & 2025-26 | 2026-27 | 2027-28 |

|---|---|---|---|

| 0 – 18,200 | Tax free | Tax free | Tax free |

| 18,201 – 45,000 | 16% | 15% | 14% |

| 45,001 – 135,000 | 30% | 30% | 30% |

| 135,001 – 190,000 | 37% | 37% | 37% |

| >190,000 | 45% | 45% | 45% |

$1,000 instant tax deduction

From 1 July 2026, Australian tax residents who earn assessable income from work will be able to claim an automatic $1,000 deduction without needing to itemise or substantiate work-related expenses.

- Taxpayers with work-related deductions above $1,000 can choose to claim the actual amount in the usual way (with substantiation).

- Charitable donations, union and professional association fees, income protection premiums, and other non-work deductions remain claimable separately, in addition to the $1,000.

- There is no requirement to keep receipts for the $1,000 standard deduction.

Working Australians Tax Offset (WATO)

A new permanent $250 Working Australians Tax Offset will apply from the 2027-28 income year. It is available to individuals deriving income from salary and wages, or as a sole trader, and is automatically delivered once a tax return is lodged.

The WATO is a non-refundable offset — it can reduce tax payable to nil but cannot generate a refund. Combined with the legislated tax cuts, it lifts the effective tax-free threshold for working Australians to approximately $19,985 (or up to $24,985 for workers also eligible for the Low Income Tax Offset).

Capital gains tax — major reform

From 1 July 2027, the 50% CGT discount will be replaced by cost-base indexation, and a 30% minimum tax rate will apply to net capital gains for individuals, trusts and partners in partnerships.

This is one of the most significant changes to capital gains taxation since the introduction of the 50% discount in 1999.

Key features

- Cost-based indexation — taxpayers will be able to index the cost base of CGT assets held for more than 12 months using a CPI methodology similar to the indexation rules that applied before 1999.

- 30% minimum tax — a 30% minimum tax rate will apply to net (indexed) capital gains made by individuals, trusts and partnerships.

- Applies to all CGT assets held by individuals, trusts and partnerships — including pre-CGT (pre-20 September 1985) assets.

- Companies are not affected — companies are not currently eligible for the 50% CGT discount.

- Superannuation funds are not affected — complying super funds (including SMSFs) continue to access the 1/3rd CGT discount on assets held more than 12 months.

- Income-support payment recipients are exempt from the 30% minimum tax (including Age Pensioners and part-pensioners).

Transitional rules

- Assets purchased and sold before 1 July 2027 — no change. The 50% discount continues to apply.

- Assets owned before 1 July 2027 and sold after — the 50% discount applies to gains accrued up to 30 June 2027; indexation and the 30% minimum tax apply to gains from 1 July 2027.

- Assets purchased on or after 1 July 2027 — entirely under the new arrangements.

- Pre-CGT assets — gains accrued before 1 July 2027 remain exempt.

Taxpayers will need to determine the market value of CGT assets as at 1 July 2027 — either by obtaining a valuation or by using an ATO-provided apportionment formula based on the asset’s holding period and growth rate.

New residential housing — investor choice

Investors in new build residential properties can choose between:

- the existing 50% CGT discount; or

- cost-based indexation combined with the 30% minimum tax.

New build properties include dwellings constructed on vacant land, or where existing properties are demolished and replaced with a greater number of dwellings. Knock-down rebuilds or renovations that do not increase supply do not qualify, nor do dwellings already occupied or previously sold.

Negative gearing — restricted to new builds

From 7.30 pm AEST on 12 May 2026, losses from established residential investment properties will no longer be deductible against an individual’s broader taxable income.

How the new rules work

- From 1 July 2027, rental losses on established residential investment properties acquired after 7.30 pm AEST 12 May 2026 will be quarantined.

- Quarantined losses can only be offset against rental income or capital gains derived from residential properties. Any excess is carried forward and applied against future residential property income or gains.

- Where there are unused losses on a property’s sale, FirstTech’s view is that those losses are included in the property’s cost base, reducing the gross capital gain on disposal.

Properties not affected

- Eligible new builds (as defined for the CGT changes above).

- Established residential properties acquired before 7.30 pm AEST on 12 May 2026 — until the point of disposal.

- Properties in widely-held trusts (for example, most managed investment trusts).

- Properties held in superannuation funds (including SMSFs).

- Established properties purchased between 12 May 2026 and 30 June 2027 can be negatively geared up to 30 June 2027, but not thereafter (transitional measure).

30% minimum tax on discretionary trusts

From 1 July 2028, a minimum 30% tax rate will apply to the taxable income of discretionary trusts.

This is a fundamental change to the way discretionary trusts (commonly referred to as family trusts) have been taxed.

How it will operate

- The trustee will pay 30% tax on the trust’s taxable income.

- Beneficiaries (other than corporate beneficiaries) will receive a non-refundable tax credit for the tax paid by the trustee.

- Trustees receiving franked dividends will be required to use franking credits to pay the minimum tax.

- Corporate beneficiaries will not receive non-refundable credits to prevent their conversion into refundable franking credits.

Excluded trusts and income

The minimum tax will not apply to:

- fixed and widely-held trusts (including fixed testamentary trusts)

- complying superannuation funds

- special disability trusts, deceased estates and charitable trusts

Excluded income types include primary production income, certain income of vulnerable minors, amounts subject to non-resident withholding tax, and income from discretionary testamentary trusts in existence at the announcement date.

Rollover relief

To assist small businesses and other taxpayers who wish to restructure out of a discretionary trust (for example, into a company or a fixed trust), rollover relief will be available for three years from 1 July 2027.

Business taxation

$20,000 instant asset write-off made permanent

From 1 July 2026, small business entities with aggregated annual turnover under $10 million will permanently access an immediate income tax deduction for the acquisition of depreciable capital assets valued up to $20,000.

The provision that prevents small business entities from re-entering the simplified depreciation regime for 5 years if they have previously opted out will remain suspended until 30 June 2027.

Loss carry-back returns

For income years commencing on or after 1 July 2026, companies with aggregated global annual turnover under $1 billion will be able to carry back a tax loss and offset it against income tax paid up to two years earlier.

- Applies to revenue (income tax) losses only.

- The company’s franking account balance limits the amount of the carry-back.

- This is a permanent reintroduction — the rules were last seen during the COVID period.

Loss refundability for small start-ups

From income years commencing on or after 1 July 2028, start-up companies in their first two years of operation with aggregated annual turnover under $10 million will be able to convert tax losses into a refundable tax offset.

The offset is limited to the value of fringe benefits tax and withholding tax on wages paid to Australian employees in the loss year.

PAYG instalments — monthly option

From 1 July 2027, small and medium businesses will have the option to:

- report and pay PAYG instalments monthly rather than quarterly; and

- use an ATO-approved calculation embedded in accounting software to calculate and vary instalments.

Research & Development Tax Incentive — recalibrated

Significant reforms apply from 1 July 2028:

- Refundable offset threshold raised from $20m to $50m aggregated turnover.

- Refundability tied to entity age — only young SMEs (under 10 years old) will access the refundable offset.

- Offset rate increases for all entities — for SMEs, the rate becomes 23 percentage points above the corporate tax rate (effective 48% for SMEs).

- For large companies, the offset rate rises from 8.5 to 13 percentage points above the corporate tax rate, and jumps to 21 percentage points when R&D intensity exceeds 1.5%.

- Removal of eligibility for supporting R&D activities — only core R&D expenditure qualifies.

- Maximum expenditure threshold raised from $150m to $200m.

- Minimum spend requirement raised from $20,000 to $50,000.

Venture capital — expanded thresholds

From 1 July 2027, the following Venture Capital Limited Partnership (VCLP) and Early Stage VCLP thresholds increase:

| Threshold | Current | From 1 July 2027 |

|---|---|---|

| VCLP — max investee asset value at investment | $250m | $480m |

| ESVCLP — max investee asset value at investment | $50m | $80m |

| ESVCLP — cap on investee total assets for full tax exemption | $250m | $420m |

| ESVCLP — maximum fund size | $200m | $270m |

The Early Stage Venture Capital Investor (ESVCI) program closes to new applications from Budget night (12 May 2026).

Foreign resident CGT regime — strengthened

Building on the 2024-25 Budget announcements, draft legislation has been introduced to:

- Clarify and broaden the definition of real property (with retrospective effect from 12 December 2006) for foreign resident CGT under Division 855.

- Amend the point-in-time principal asset test to a 365-day testing period.

- Require foreign residents disposing of shares and other membership interests valued at $50m or more to notify the ATO before executing the transaction.

A 50% CGT discount will apply to disposals on or before 30 June 2030 for foreign residents investing in Australian renewable energy assets.

Corporate reporting relief — larger threshold for proprietary companies

Thresholds for determining whether a proprietary company is ‘large’ and therefore required to lodge an audited annual financial report, directors’ report and sustainability report are being increased:

- Consolidated revenue threshold: $50m → $100m

- Consolidated gross assets threshold: $25m → $50m

International tax — Pillar Two side-by-side package

Consistent with other OECD/G20 jurisdictions, Pillar Two will be amended to implement the side-by-side package, applying from 1 January 2026.

Superannuation

Division 296 — extra tax on balances above $3 million

From 1 July 2026, Division 296 imposes additional tax on the earnings of individuals with total super balances (TSBs) above $3 million. First assessments will be issued after 30 June 2027 based on the 2026-27 income year.

How Division 296 will operate

- An additional 15% tax on earnings attributable to the portion of an individual’s TSB above $3 million.

- A further 10% tax (totalling 25% extra) on earnings attributable to the portion of TSB above $10 million.

- Assessed to the individual, not the super fund. The individual can elect to pay personally or have the amount released from super.

- The rules apply to realised capital gains accrued from 1 July 2026 onwards, with mechanics varying by fund type.

- Special provisions cover indexation of the thresholds, treatment on death, and transitional relief in the 2026-27 year.

Payday Super begins 1 July 2026

From 1 July 2026, employers will generally be required to pay Super Guarantee (SG) contributions at the same time as salary and wages, rather than quarterly.

Supporting changes include amendments to the earnings base used to calculate SG and the SG charge, as well as changes to how the Maximum Contributions Base is calculated and applied.

Fringe Benefits Tax — Electric vehicle discount

The Government is transitioning the FBT exemption for electric vehicles (EVs) towards a more sustainable long-term setting. Each phase will be grandfathered.

| Phase | Period | Treatment |

|---|---|---|

| Phase 1 | Until 31 March 2027 | Existing 100% FBT exemption continues for eligible EVs |

| Phase 2 | 1 April 2027 – 31 March 2029 | EVs ≤ $75,000: 100% FBT discount continues; EVs > $75,000 (up to LCT threshold): 25% FBT discount via 15% statutory formula rate |

| Phase 3 | From 1 April 2029 | Permanent 25% FBT discount for all EVs valued up to the fuel-efficient LCT threshold (currently $91,387) via 15% statutory formula rate |

An eligible vehicle retains the treatment that applied when the arrangement commenced.

Households, health and social support

Cost-of-living measures

- Fuel excise was more than halved, and the heavy-vehicle road user charge was reduced to zero for three months from 1 April 2026 — part of a $2.9 billion package.

- $1 billion Economic Resilience Program — interest-free loans through the National Reconstruction Fund for manufacturing and logistics businesses impacted by the Middle East conflict.

- $5.9 billion in additional spending on the Pharmaceutical Benefits Scheme to list more medicines.

- Medicare Urgent Care Clinics made permanent — $1.8 billion over five years.

Housing

- $5.9 billion extra for the Help to Buy program for first home buyers.

- $2 billion for housing-enabling infrastructure.

- $500 million to streamline environmental approvals to support construction.

- Extension of the ban on foreign purchases of established dwellings.

Aged care and home care

- $3.7 billion aged care package — up to 5,000 additional residential aged care beds per year, principally for those with limited financial means.

- New capital subsidies for aged care providers and changes to the Accommodation Supplement.

- Up to 20 additional Specialist Dementia Care units.

- Fully funded personal care services (showering, dressing, incontinence aids) under the Support at Home program.

- Faster access to Support at Home places, improved assessments and end-of-life pathways.

Private Health Insurance Rebate — age-based uplift removed

From 1 April 2027, the age-based uplift to the Private Health Insurance Rebate is being removed, saving $3.0 billion over four years. Under current rules, policyholders aged 65–69 and 70+ receive higher rebate percentages than younger policyholders at the same income level. Those savings are being redirected to aged care.

Social Security and Services Australia

- $2.2 billion for Services Australia over five years — frontline staff, cyber security uplift, and improvements to myGov.

- Pension Supplement to overseas recipients — full rate extended from 6 to 12 weeks during temporary absences; ceased after 12 weeks of temporary absence or upon permanent departure—estimated savings of $218 million over five years.

- Increased Medicare levy low-income thresholds from 1 July 2025.

Trade, industry and innovation

Trade and customs

- Abolition of a further 497 nuisance tariffs from 1 July 2026, taking the cumulative total abolished to approximately 1,000 — estimated to reduce compliance costs by $157m per year.

- $7.6 million to expand the Australian Trusted Trader program.

- $7.5 billion Fuel and Fertiliser Security Facility — supply chain commitments with Japan, Korea, Singapore, Malaysia and Brunei.

- 20% domestic gas reservation for LNG exporters from 1 July 2027, alongside the removal of the Australian Domestic Gas Security Mechanism.

- $55 million Transport Resilience and Capacity Kickstart pilot — incentivising rail and sea freight.

Skills, AI and digital adoption

- $85.2 million to accelerate skills assessments for migrant trades workers.

- Australian Apprenticeships Incentive System reformed from 1 January 2027 — employer incentives prioritised for small and medium employers and Group Training Organisations.

- Round 3 of the Digital Solutions program launches on 1 July 2026 with a new AI and emerging technology focus.

- Up to $70 million in AI Accelerator grants via the Cooperative Research Centres program.

Science and innovation

- $1.5 billion invested in CSIRO, the National Measurement Institute and the Square Kilometre Array.

- $508.5 million to increase disbursements from the Medical Research Future Fund.

Establishment of a new National Resilience and Science Council to coordinate public innovation investment.

ATO activity and compliance

The Australian Taxation Office will receive an additional $86.3 million over four years from 1 July 2026, and $9.7 million per year ongoing from 2030-31, to expand its compliance activities.

Targeted compliance areas include:

- Phase 2 of the Counter Fraud Strategy — modernising fraud prevention and detection across the tax and super system, including fraud by tax agents and intermediaries.

- Targeted exceptions to tax secrecy and enhanced information-gathering powers.

- Two-year R&D Tax Incentive compliance project.

The Budget also includes funding to strengthen governance and ASIC supervision of managed investment schemes ($17.8 million over four years), and to explore extending the Consumer Data Right to enable taxpayers to share ATO-held data with their advisers.

The economy

The 2026-27 Budget is framed against an uncertain global backdrop. For households and businesses alike, the outlook remains challenging: interest rates, inflation and unemployment — the metrics that most acutely shape economic confidence — are all moving in the wrong direction.

The Government delivered an underlying cash deficit of $31.5 billion for 2026-27, forecast to widen slightly to $34.4 billion before narrowing to $25.3 billion by 2029-30. The budget position over the forward estimates has improved by $44.9 billion compared with the December MYEFO, supported by:

- modest revenue upgrades from higher commodity prices and elevated inflation; and

- $63.8 billion in announced savings, including the removal of the age-based Private Health Insurance Rebate uplift and changes to the Pension Supplement for overseas recipients.

Global growth remains subdued. The Middle East conflict has triggered supply-chain dislocation in fuel, fertiliser and freight, prompting the new Fuel Resilience package and Economic Resilience Program. Trade tensions and Australia’s exposure to the China-United States trade relationship continue to weigh on the outlook for trade-exposed sectors.

Industry response

The Budget’s tax reform agenda has attracted strong commentary across the accounting and advisory profession.

CPA Australia has described the changes as a “tax grab” that “punishes aspiration and deters investment”, warning that the combination of CGT and discretionary trust changes effectively creates a “minimum tax on aspiration” for those investing or building a business.

Grant Thornton has highlighted the volume of measures — particularly the welcome increases to the venture capital thresholds — but notes that the increased complexity around the CGT transitional rules will require careful planning by 1 July 2027.

Colonial First State (FirstTech) notes that the 30% minimum tax on capital gains means the long-standing strategy of realising gains in years of reduced income (such as after retirement) may no longer be as effective — unless the client also qualifies for an income support payment.

What this means for you

The 2026-27 Budget contains genuinely significant changes that will affect tax planning, investment, business structuring and retirement strategies. Many of the most important measures do not commence until 1 July 2027 or later, which provides time to plan, but also creates important review points.

Key considerations between now and 1 July 2027

- Property investors — review the timing of any planned acquisitions or disposals of established residential property, and consider whether new build properties may better suit your strategy going forward.

- Investors holding CGT assets — consider the impact of the move from a 50% discount to indexation with a 30% minimum tax, and ensure asset values at 1 July 2027 can be substantiated.

- Family trust beneficiaries — review distribution patterns in light of the 30% minimum trust tax from 1 July 2028. Some clients may benefit from a restructure (with rollover relief available for three years from 1 July 2027).

- Business owners — model the impact of the permanent $20,000 instant asset write-off, the return of loss carry-back, and the revised R&D Tax Incentive thresholds.

- High-balance super members — finalise planning for Division 296 — including reviewing investment strategy, drawdown patterns and the choice between paying personally or releasing the liability from super.

- Employers — ensure your payroll and super systems are ready for Payday Super on 1 July 2026 and the new $1,000 standard deduction for employees from 1 July 2026.

- EV salary packaging — clients considering an EV novated lease should be aware of the FBT phase-down from 1 April 2027.

We’re here to help

The AAG team is well placed to help you and your business navigate the changes announced in the 2026-27 Federal Budget. If you would like to discuss how any of these measures affect your circumstances, please get in touch with us.

Important information

This newsletter is a summary of measures announced in the 2026-27 Federal Budget on 12 May 2026 and is based on information available as at the date of publication. It is general in nature and does not constitute personal financial, tax or legal advice. Many measures require legislation and remain subject to passage through Parliament. Before acting on any information in this newsletter, you should consider your own circumstances and seek professional advice from your AustAsia Group adviser. Source materials include Commonwealth of Australia Budget Papers, and commentary from Grant Thornton Australia, Colonial First State, CPA Australia, RSM Global and TaxBanter (Knowledge Shop).