A number of measures aimed at reducing tax avoidance options available to multinational organisations have been announced.

Companies to declare their subsidiaries. (From 1 July 2023)

New reporting requirements from 1 July 2023 will require the following:

- Australian public companies (listed and unlisted) to disclose information on the number of subsidiaries and their country of tax domicile;

- Tenderers for Australian Government contracts worth more than $200,000 to disclose their country of tax domicile (by supplying their ultimate head entity’s country of tax residence); and

- Large multinationals, defined as significant global entities, prepare for public release of certain tax information on a country-by-country (CbC) basis and a statement on their approach to taxation for disclosure by the ATO.

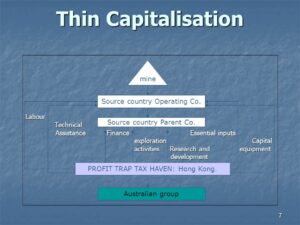

Thin cap rules introduce an earnings-based test (From 1 July 2023)

The thin capitalisation rules, which can potentially limit the amount that can be claimed for debt deductions such as interest, will be amended. The Government will replace the current safe harbour and worldwide gearing tests with earnings-based tests to limit debt deductions in line with an entity’s profits.

The thin capitalisation rules, which can potentially limit the amount that can be claimed for debt deductions such as interest, will be amended. The Government will replace the current safe harbour and worldwide gearing tests with earnings-based tests to limit debt deductions in line with an entity’s profits.

Applying to multinational entities operating in Australia and any inward or outward investor, in line with the existing thin capitalisation regime, the measures will:

• Limit an entity’s debt-related deductions to 30 per cent of profits (using EBITDA as the measure of profit). This new earnings-based test will replace the safe harbour test.

• Allow deductions denied under the entity-level EBITDA test (interest expense amounts exceeding the 3% EBITDA ratio) to be carried forward and claimed in a subsequent income year (up to 15 years).

• Allow an entity in a group to claim debt-related deductions up to the worldwide group’s net interest expense level as a share of earnings (which may exceed the 30% EBITDA ratio). This new earnings-based group ratio will replace the worldwide gearing ratio.

• Retain an arm’s length debt test as a substitute test which will apply only to an entity’s external (third party) debt, disallowing deductions for related party debt under this test.

Financial entities will continue to be subject to the existing thin capitalisation rules.

The current thin capitalisation regime limits debt deductions up to the maximum of three different tests:

- A safe harbour (debt to asset ratio) test;

- An arm’s length debt test; and

- A worldwide gearing (debt to equity ratio) test.

Global entities denied deductions for intangibles. (From payments made on or after 1 July 2023)

Significant global entities (at least $1bn global revenue) will no longer be able to claim a tax deduction for payments made, directly or indirectly, to related parties for intangibles held in low or no-tax jurisdictions. This could include royalties paid for the use of trademarks and other intellectual property items.

Significant global entities (at least $1bn global revenue) will no longer be able to claim a tax deduction for payments made, directly or indirectly, to related parties for intangibles held in low or no-tax jurisdictions. This could include royalties paid for the use of trademarks and other intellectual property items.

A low or no tax jurisdiction is one with:

- A tax rate of less than 15%, or

- A tax-preferential patent box regime without significant substance.

The measure is anticipated to apply to payments made on or after 1 July 2023.

This measure could impact Australian entities that are subsidiaries of a foreign parent entity where the global revenue of the consolidated group for accounting purposes is $1bn or more.

Removed: Self-assessment of intangible assets

Announced in the 2021-22 Budget and due to commence on 1 July 2023, the measure enabling taxpayers to self-assess the effective life of certain intangible assets, rather than being required to use the effective life currently prescribed by statute, has been removed.

The measure was to apply to assets acquired from 1 July 2023, including patents, registered designs, copyrights and in-house software.

Dramatic jump in penalties for competition and consumer law breaches (From 2022-23 financial year)

From the 2022-23 year, the penalties for a corporation breaching competition and consumer laws will increase sharply from a maximum of $10m to a maximum of $50m per breach and from 10% of annual turnover to 30% of turnover (whichever is greater) during the period the breach took place.

Energy efficiency grants for SMEs (From the 2022-23 financial year)

The Government will provide $62.6m over three years from 2022-23 to help small and medium business fund energy-efficient equipment upgrades. The funding will support studies, planning, equipment and facility upgrade projects that will improve energy efficiency, reduce emissions or improve the management of power demand. No details of the grants are currently available.

Delayed: Ridesharing reporting requirements.

In the 2019-20 Mid-Year Economic and Fiscal Outlook (MYEFO), new reporting measures were announced, requiring sharing-economy online platforms to report identification and income information on participating sellers to the ATO for data matching purposes. These measures have now been delayed from:

In the 2019-20 Mid-Year Economic and Fiscal Outlook (MYEFO), new reporting measures were announced, requiring sharing-economy online platforms to report identification and income information on participating sellers to the ATO for data matching purposes. These measures have now been delayed from:

- 1 July 2022 to 1 July 2023 for transactions relating to the supply of ride-sourcing and short-term accommodation, and

- 1 July 2023 to 1 July 2024 for all other reportable transactions (including but not limited to asset sharing, food delivery and tasking-based services).