23 June 2026 announced · 25 June 2026 passed both Houses · Royal Assent pending · Ban commences 45 days after Assent

What has happened

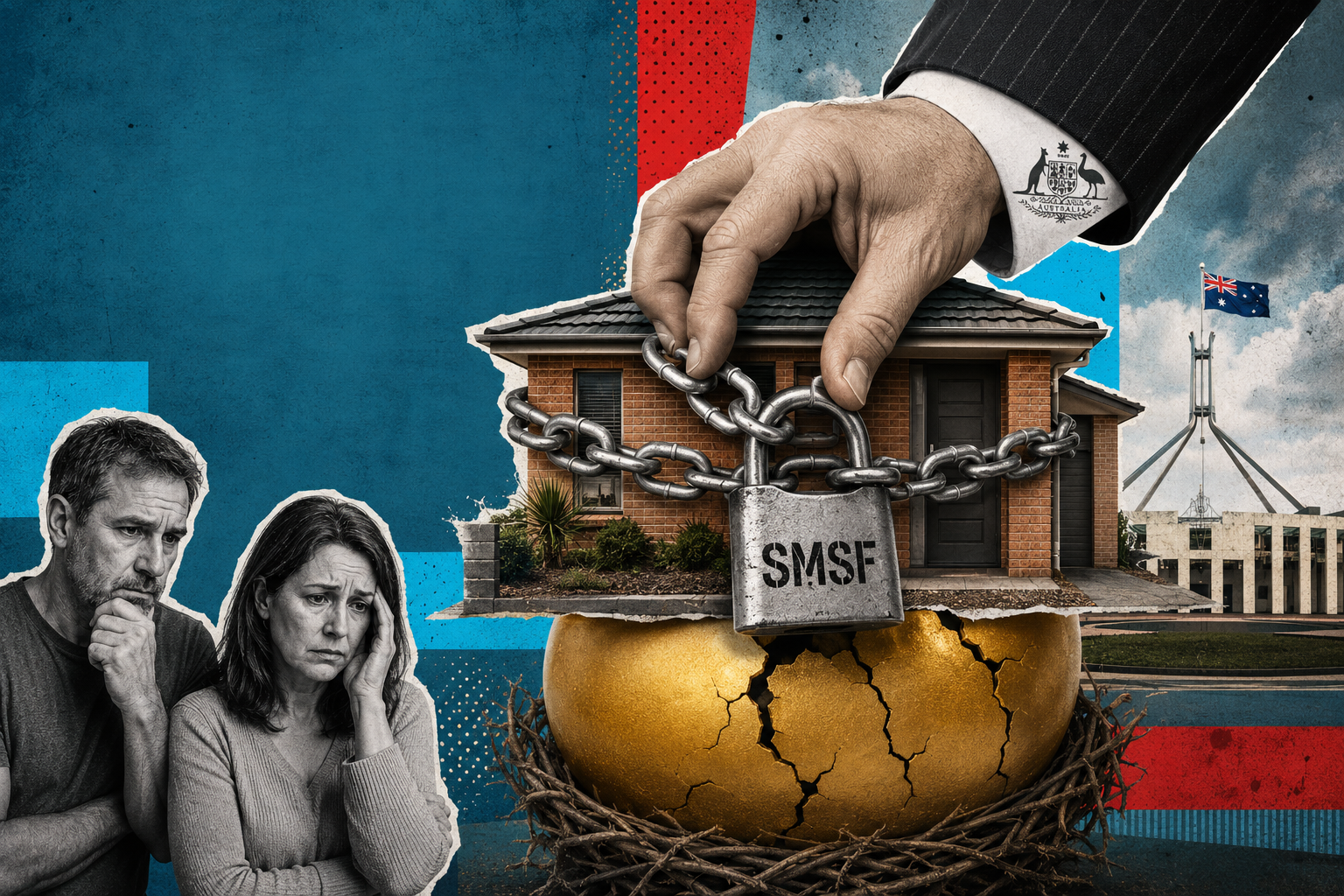

In a late-stage amendment to the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026, the Government agreed with the Australian Greens on 23 June 2026 to ban Self Managed Superannuation Funds (SMSFs) from entering into new Limited Recourse Borrowing Arrangements (LRBAs) to acquire residential property.

The Senate passed the amended bill on 25 June 2026 by 35 votes to 25, and the House of Representatives agreed to the Senate amendments later that day. At the time of writing, the Bill is awaiting Royal Assent, which is expected imminently.

The ban will commence 45 days after Royal Assent is granted. If Royal Assent is received in late June or early July 2026, this would place the operative start date around mid-August 2026. The change is inserted into the Superannuation Industry (Supervision) Act 1993 (SIS Act) as a new condition on permitted LRBAs under subsection 67A(2), effectively restricting borrowing to Business Real Property only.

Key dates

Any contract exchanged before commencement is grandparented, even if settlement is later. Existing LRBAs are fully protected; no action is required to maintain grandparenting.

What is and is not affected

Grandparenting (previously called grandfathering): the key protection

Existing LRBAs in place at commencement are fully grandparented and will not be unwound. The critical protection for anyone mid-process is that acquisitions entered into (i.e. contracts exchanged) before the commencement date are protected, even if settlement occurs after the ban takes effect. If you are currently acquiring residential property via an SMSF LRBA and have not yet exchanged contracts, time is extremely short.

The unanswered question: what is “residential”?

The most important word in the entire announcement has not yet been defined in draft legislation, and the definition matters enormously in practice. The ban is framed around “residential property”, but in SMSF legislation that concept is not always determined by zoning or title.

Consider a property that is residentially zoned under local council zoning and titled as residential on a title search, but used in practice as a medical or professional premises: a GP clinic, a psychology practice, a physiotherapy studio, a small accounting office.

Under existing SMSF rules, many of these properties already qualify as Business Real Property (BRP) despite their title and zoning, because the operative test is whether the property is used wholly and exclusively in a business. If the ban is framed around BRP as the permitted carve-out (which the SIS Act amendments appear to confirm), what falls inside or outside the ban will be determined by the actual use and business connection of the property, not by zoning alone.

Three possible definitions, three different outcomes

These three definitions do not lead to the same outcome. A property can be residential on the title, residential under local zoning, and still be treated very differently under SMSF legislation. The difference could determine whether the Business Real Property carve-out survives the legislative drafting cleanly, or whether it creates grey zones that the ATO will later need to rule on.

The political context

This measure was not the product of a housing policy review, a Treasury white paper, or any published evidence base. It was extracted by the Greens as the price of their Senate support for the Government’s broader budget package. The Treasurer acknowledged the fiscal yield is approximately $50 million over the forward estimates, a rounding error relative to the $1.06 trillion in SMSF assets. The measure is, by any objective measure, political symbolism rather than structural reform.

The argument that SMSFs using LRBAs are inflating residential property prices and crowding out first home buyers does not survive serious scrutiny. SMSFs account for less than 1% of total residential property borrowing in Australia. The change removes a low-risk, well-regulated form of leveraged investment from the retirement savings landscape while leaving higher-risk alternatives untouched. It also has no effect on property supply.

We are not suggesting clients panic. We are suggesting that the most important action right now is to understand where your SMSF arrangements sit, and to take advice before the ~10 August 2026 commencement date if you are considering any LRBA activity.

Our recommendation

- If you have an existing residential LRBA, no immediate action is required: your arrangement is grandparented.

- If you are mid-process on a residential LRBA and have not yet exchanged contracts, contact us immediately; the ban commences 45 days after Royal Assent, which is expected very soon.

- If your SMSF holds or is considering commercial property or Business Real Property, the ban does not affect you.

- If you have any questions about how your SMSF is structured in light of these changes, please call us before taking any action.

Talk to us before you act