The Government has announced that they intend to change to tax concessions on certain superannuation accounts if you have a total super balance of more than $3 million. While it is important to understand that this is just a proposal at this time, you may have some questions about whether this proposal could apply to you.

Note: At this stage, the measure is a proposal only and has not been made law.

The information included below is based on the announcement made on 28 February 2023 by the Government and a Factsheet that Treasury has since released with some additional information.

The Government intends to consult further on this proposal, and other changes may be made.

What is proposed to change?

Currently, tax on investment earnings within the accumulation phase of superannuation is at a maximum rate of 15%. It is proposed that for certain individuals with a ‘total super balance’ (TSB) that exceeds $3 million, an additional tax of 15% will apply on a portion of ‘accumulation’ account earnings.

An accumulation account is a superannuation account that you have before retirement or commencing an account-based pension, which may receive personal, employer and other contributions.

If your total super balance is less than $3 million, this change will not impact you, and investment earnings on your accumulation balance will continue to be taxed at the maximum rate of 15%.

The proposed change will not apply to earnings in a ‘retirement phase pension’, where earnings are taxed at 0%. For more information about these accounts and the separate limit called the ‘transfer balance cap’ that applies to these types of accounts, see ato.gov.au

The following table reflects the calculation of the tax required:

| Member TSB | Rate of tax on earnings |

| $0 — $1.9 million | 0% (pension); 15% (accumulation) |

| $1.9 million — $3 million | 15% (all accounts) |

| $3 million and above | 30% (all accounts) |

What is 'total super balance?'

Generally, your TSB is the sum of all amounts you have in the superannuation system (certain exceptions apply*). At a high level, it includes:

- your accumulation account balances

- your superannuation pension accounts, and

- In certain circumstances, the outstanding balance of a Limited Recourse Borrowing Arrangement (if you have a self-managed super fund that has borrowed to invest).

* Exceptions and modifications may apply, for example, if you’ve made a personal injury contribution to super. Calculating TSB can be complex, so it is essential to seek advice.

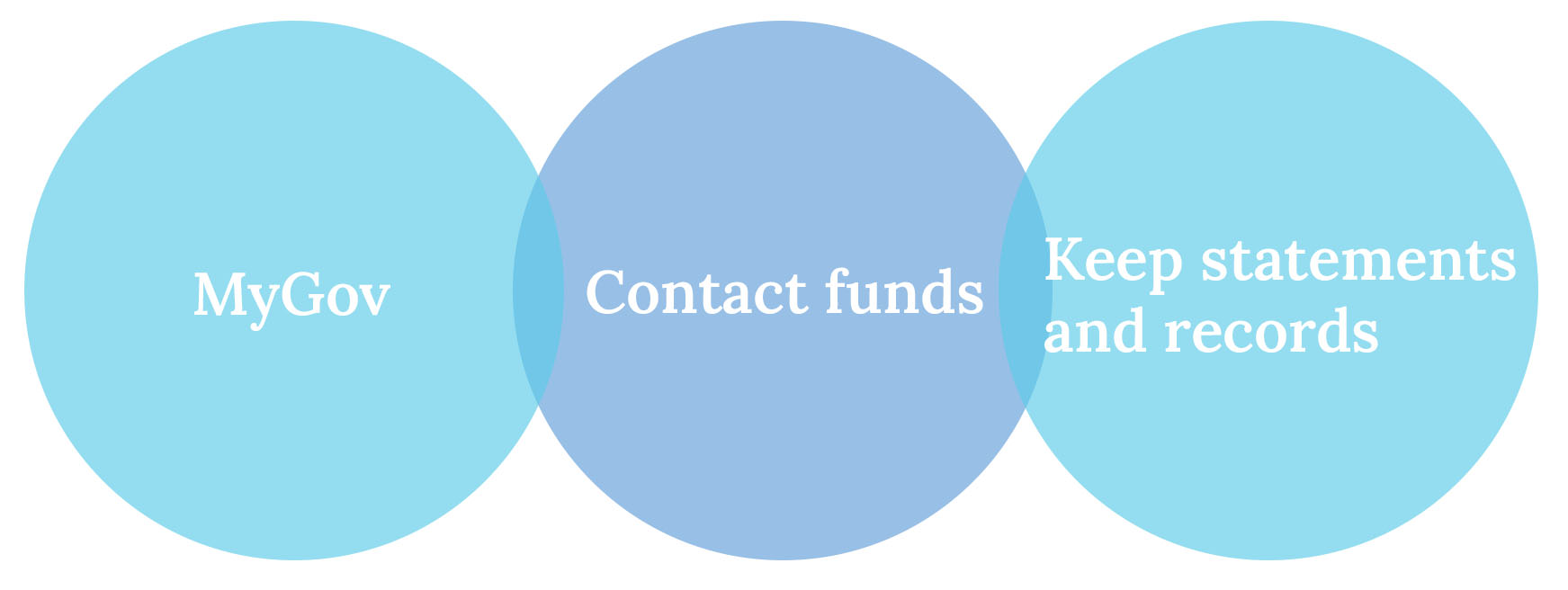

There are a few ways you can track your TSB. A valuable source of information is your MyGov account. Other options include contacting your superannuation funds and reviewing your fund’s statements and records. When reviewing your annual statement, the TSB figure your fund reports to the ATO is usually referred to as ‘exit value’ or ‘withdrawal benefit’. This may be different to the 30 June ‘closing balance.’

When will this change start?

At the moment, this is a proposal only. Based on the information released by the Government, it is currently intended that this change will commence on 1 July 2025 and that notices of additional tax liability will first be sent in the 2026/27 financial year. The law will need to pass to implement the proposal. Also, some of the details about the proposal may change.

How will earnings on my account be determined and any tax liability calculated?

To simplify the process and to ensure additional reporting requirements and system changes don’t burden superannuation funds, a simplified method has been proposed to calculate fund earnings and any resulting tax liability. Broadly, this looks at your TSB at the beginning and end of the year and any contributions and

withdrawals you’ve made during the year. Once your earnings have been determined using this simplified method, another formula will be applied to determine how much of these earnings relate to your accumulation account before tax is applied on this amount at a rate of 15%.

If you don’t have any earnings and are instead assessed as having a loss for the year, it has been proposed that you’ll be able to carry this loss forward to a future year to offset a tax liability you may have in the future under this proposed regime.

More detail about this formula and some worked examples can be found on the Treasury’s Factsheet

How will the additional tax be paid, and will I need to report my balances to the ATO?

The ATO will use data from superannuation funds to determine who is liable for the additional tax and the amount of tax payable. The ATO is expected to issue tax notices when the time comes, separate from personal income tax. There is limited detail on how the measure will work, and the Government will consult further on practical implementation issues.

Can I withdraw any of my superannuation to reduce my balance below $3 million?

Unless you’ve met a ‘condition of release, ’ the information made available on this proposal does not indicate that you’ll be able to withdraw any amounts from super to prevent the additional tax. Super law limits the conditions under which you can access your funds. Generally, this is limited to when you reach age 65, meet the definition of retirement, and in certain other limited and exceptional circumstances when you’re in financial hardship. For more information about conditions of release, see ato.gov.au

What if I have more than one fund?

As explained above, TSB considers the sum of all your superannuation interests, including your accumulation accounts and superannuation income streams. The $3 million threshold is cumulative, meaning it is not a limit per super fund but instead looks at your combined balances.

How will the additional tax be paid?

The Government’s factsheet indicates that the excess tax can be paid:

- directly by you to the ATO, or

- by making an election to release the funds from the super.

You can select the fund from which the tax is paid if you hold multiple funds.

I have a defined benefit fund. Will this apply to me?

Yes. The Government intends to include defined benefit funds in the measure. However, because defined benefit funds operate differently from other types of super funds, such as public offer funds and self-managed super funds (SMSFs), there will need to be further discussion with the industry to work out how defined benefit funds will be captured.

I have an SMSF. Will this apply to me?

Yes. There is no exemption for Self Managed Super Funds.

Should I make any changes now to my retirement savings strategy and is superannuation still worthwhile?

For many people with super savings above $3 million, superannuation may still offer concessional tax rates on earnings when compared to your marginal rate of tax, which could be as high as 47%. It is essential to understand that the answer to this question will differ for everyone and may even change as your circumstances change.

There are other potential benefits to superannuation, aside from what, for many, is a concessional tax rate on earnings. It is important to remember that this is currently a proposal only, and if formally made law, some of the final details relating to this measure may change from what has been announced.

Please contact us if you’d like more information about how this proposal could apply to you if it does become law and to ensure the strategies you put in place are right for you.