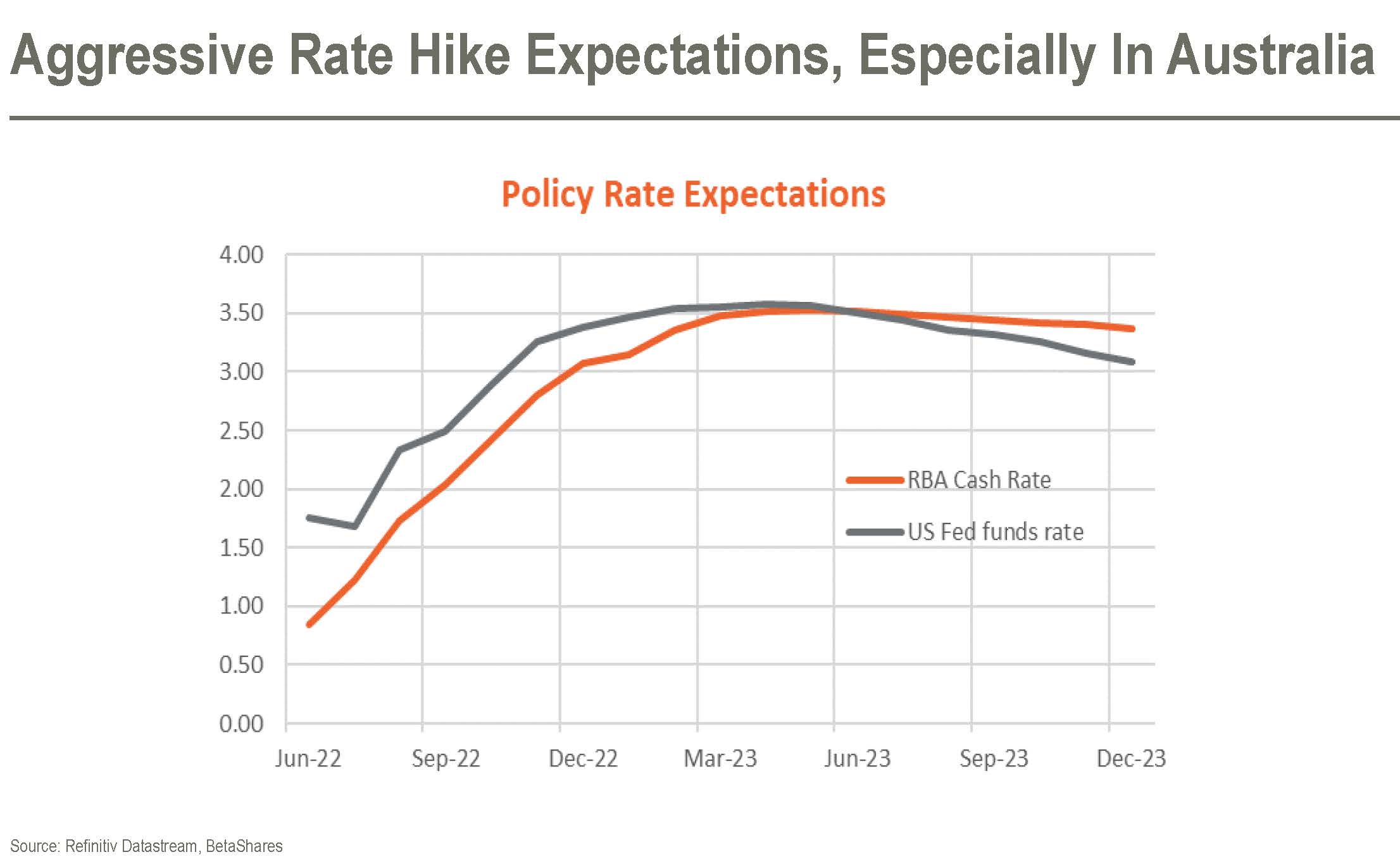

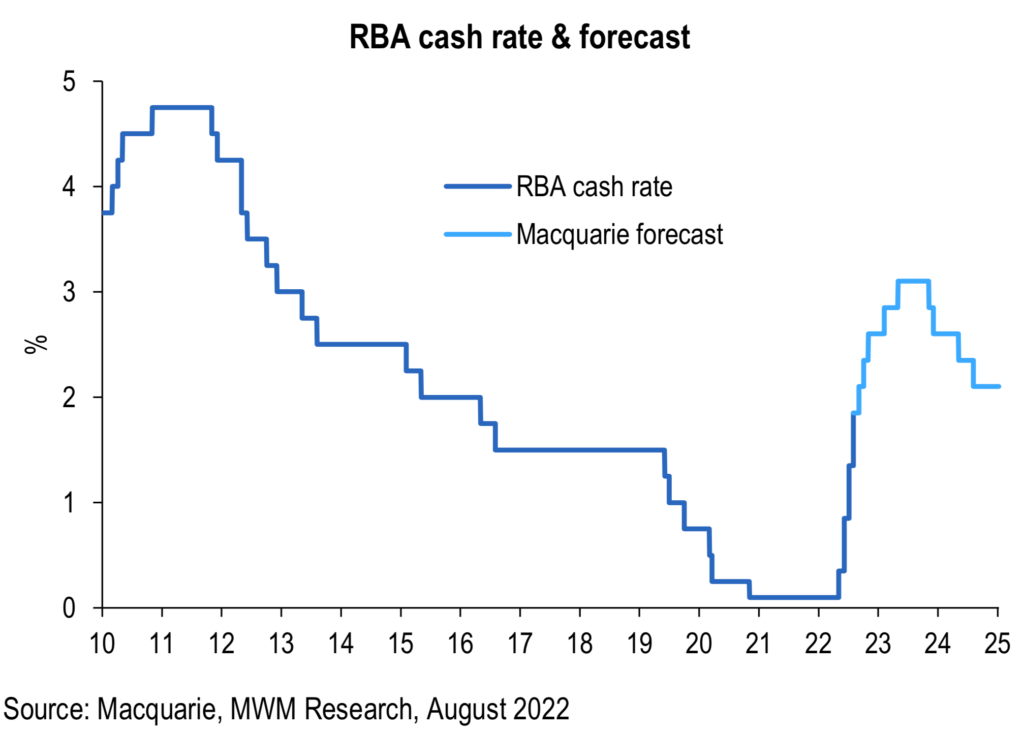

The RBA lifted the cash rate to 1.85% in early August 2022. The increase comes a few weeks after Reserve Bank Governor Philip Lowe told the Australian Strategic Business Forum that “… we’re going through a process now of steadily increasing interest rates, and there’s more of that to come. We’ve got to move away from these very low levels of interest rates we had during the emergency.” He said that we should expect interest rates of 2.5% – how quickly we get there depends on inflation.

The RBA Governor has come under increasing pressure over comments made in October 2021 suggesting that interest rates would not rise until 2024. At the time, however, Australia was coming out of the Delta outbreak, wage and pricing pressure was subdued, and inflation was low. That all changed and changed dramatically. Inflation is now forecast to reach 7.75% over 2022 before trending down. We’re not expected to reach the RBA’s target inflation rate range of 2% to 3% until the 2023-24 financial year.

In the UK, the situation is worse, with the Bank of England predicting that inflation will reach around 13% over the next few months. The UK has been heavily impacted by the war in Ukraine, with the price of gas doubling, compounding pressure from post-pandemic supply chain issues and price increases.

With interest rates rising, what can we expect?

Deputy RBA Governor Michele Bullock recently said that Australia’s household credit-to-income ratio is a relatively high 150%, increasing in an environment that enables households to service more elevated debt levels.

But it is not all doom and gloom. “Strong growth in housing prices over 2021 and early 2022 has boosted asset values for many homeowners, with housing assets now comprising around half of the household assets,” she said. The recent downturn in house prices has only marginally eroded the significant increases over recent years. Plus, households have saved around $260m since the pandemic creating a buffer for rising interest rates. This, however, is a macro view of the economy at large, and individual households and businesses will face different pressures depending on their circumstances.

But it is not all doom and gloom. “Strong growth in housing prices over 2021 and early 2022 has boosted asset values for many homeowners, with housing assets now comprising around half of the household assets,” she said. The recent downturn in house prices has only marginally eroded the significant increases over recent years. Plus, households have saved around $260m since the pandemic creating a buffer for rising interest rates. This, however, is a macro view of the economy at large, and individual households and businesses will face different pressures depending on their circumstances.

For businesses, the rate increase has a twofold effect. It is not just the rate rise and the higher cost of funds in their borrowings. That is significant, but at this stage, if anything, it is a lesser issue. The more significant impact comes from negative consumer sentiment and the flow-through effect on sales and cash flow.

- Generally, your debts should not exceed 35-40% of your assets. There will be exceptions to this with new business start-ups and first home buyers.

- Review the cost of cash in your business, reviewing rates, and the configuration and mix of loans to ensure you are not paying more than you need to.

- If possible, avoid having private debt and business and investment debts. You can’t get tax relief on your personal debt.

- Keep an eye on debtors, and don’t become your customer’s bank.