Further to our recent article on the Property Market and our views of the fundamentals, Macquarie Bank released its own Housing Market Update for at the end of August 2023.

For those that missed our article in mid July 2023, please see it here:

The Australian Residential Property Market

The article provides 5 main trends / topics for the property market, being as follows:

- Property rebound is losing momentum

- Despite reaching the ‘fixed-rate cliff’, mortgage arrears remain in check

- Rental market to remain tight

- Despite strong rental conditions, more investors are selling

- Development pipeline lacks approved supply

It is a great read, and gives a lot of background for where the Industry sees the market, rather than the political rhetoric that is in the media.

The Macquarie Bank article gives a great background and a different view on the market. We have reproduced the article in its entirety.

If you have any concerns on your position or want specific advice to your circumstance, please contact us so that we can help you with your concerns and help to develop a solution that suits your requirements.

5 trends in Australia’s shifting housing market

Housing market update August 2023

1. Property rebound is losing momentum

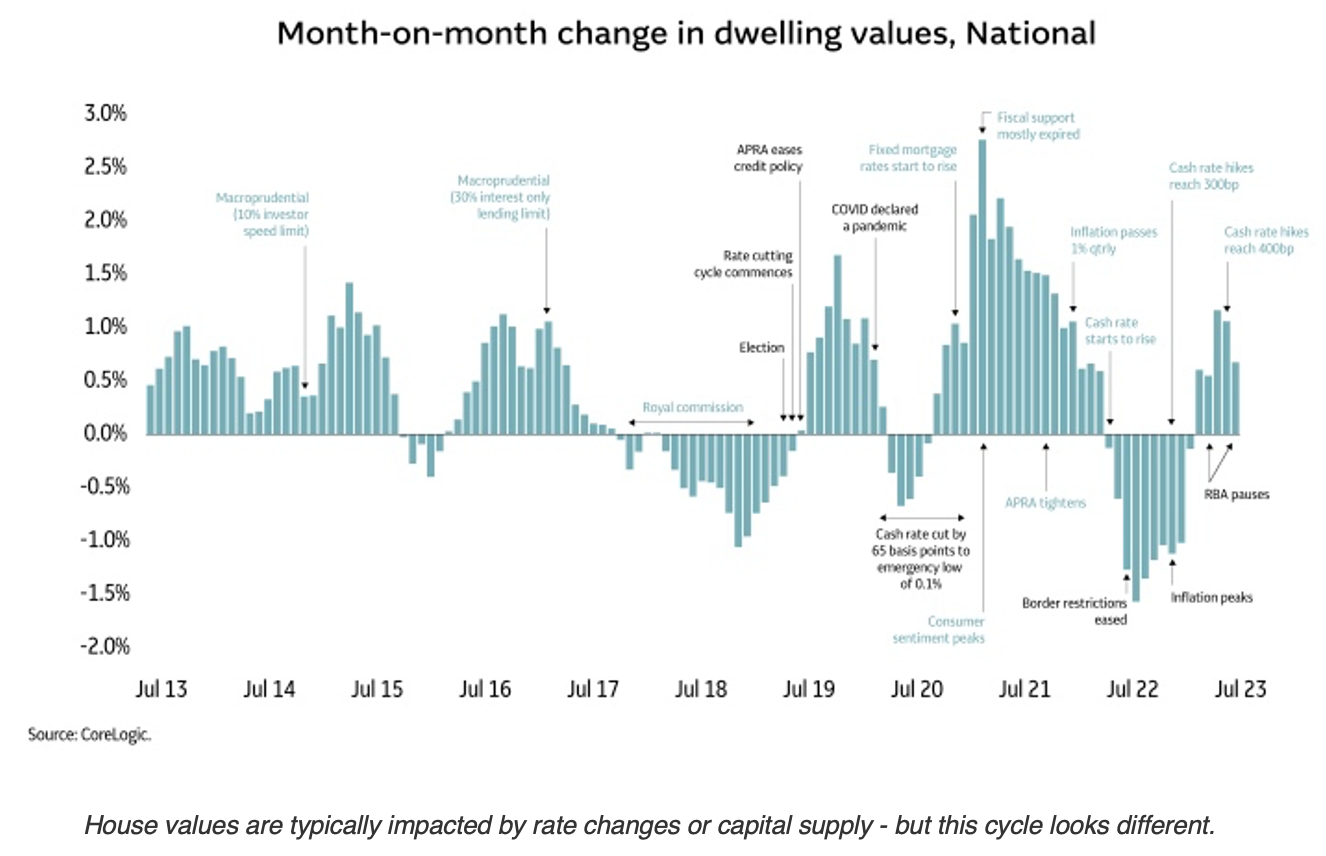

The property market has been on a rollercoaster ride over the past couple of years, defying typical growth cycles.

“We moved through a period of nearly 30% growth in our national index between 2020 and mid-2022, which was the fastest growth cycle on record. Then we experienced a 9% drop between May 2022 and early 2023, which again, was one of the fastest drops over a relatively short period of time. And now we’re back into this new phase of a positive inflection in housing values,” explained Lawless.

The recent rebound in Australian property prices has defied expectations in the midst of tightening policy. One key factor in Australia’s recent rebound is extraordinarily low supply amidst average levels of demand.

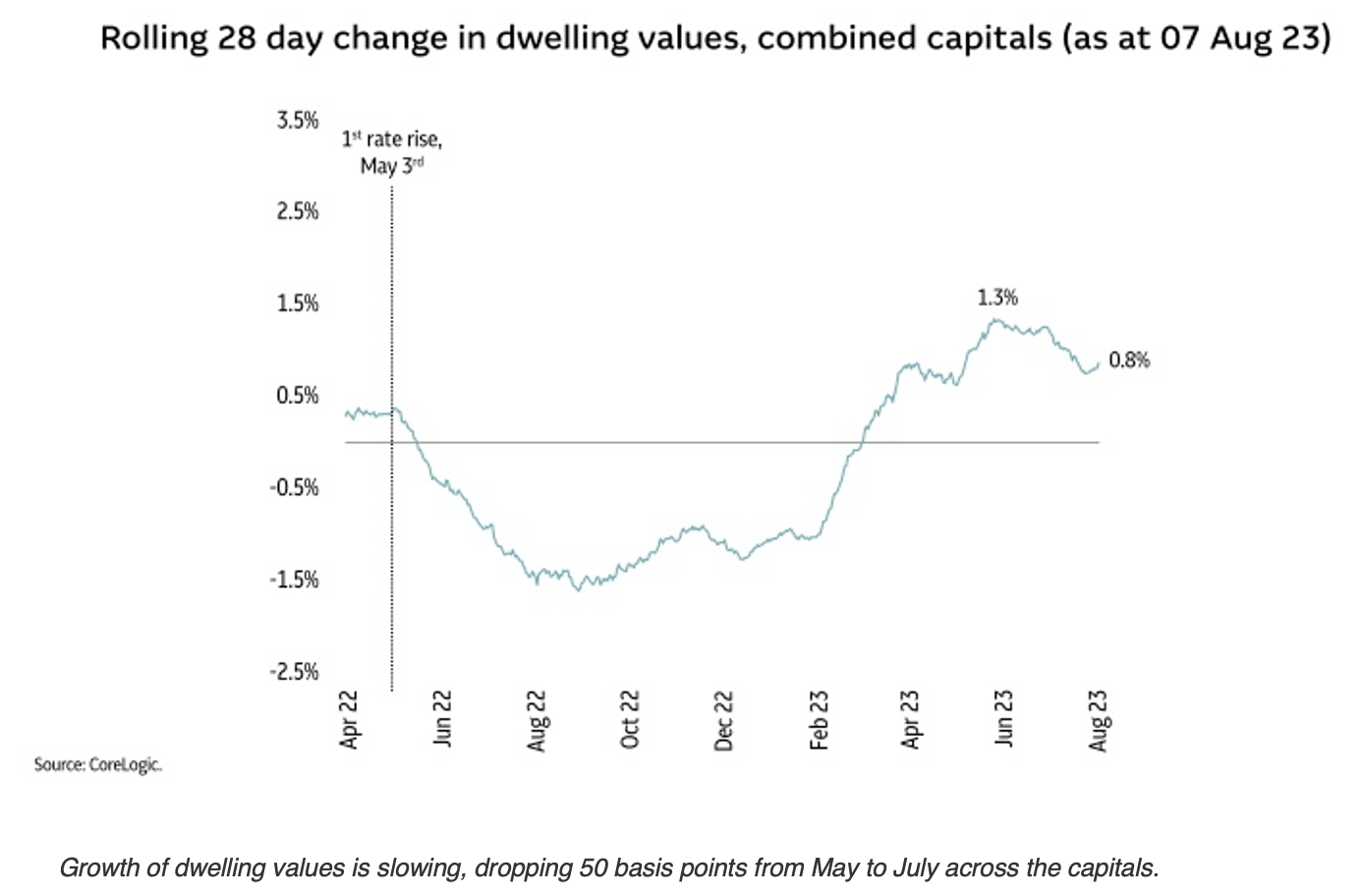

As new listings start to pick up, growth in the market appears to be easing in most regions. While July marked the fifth consecutive month of growth, property values across the country rose only 0.8% compared to 1.3% in May 2023.

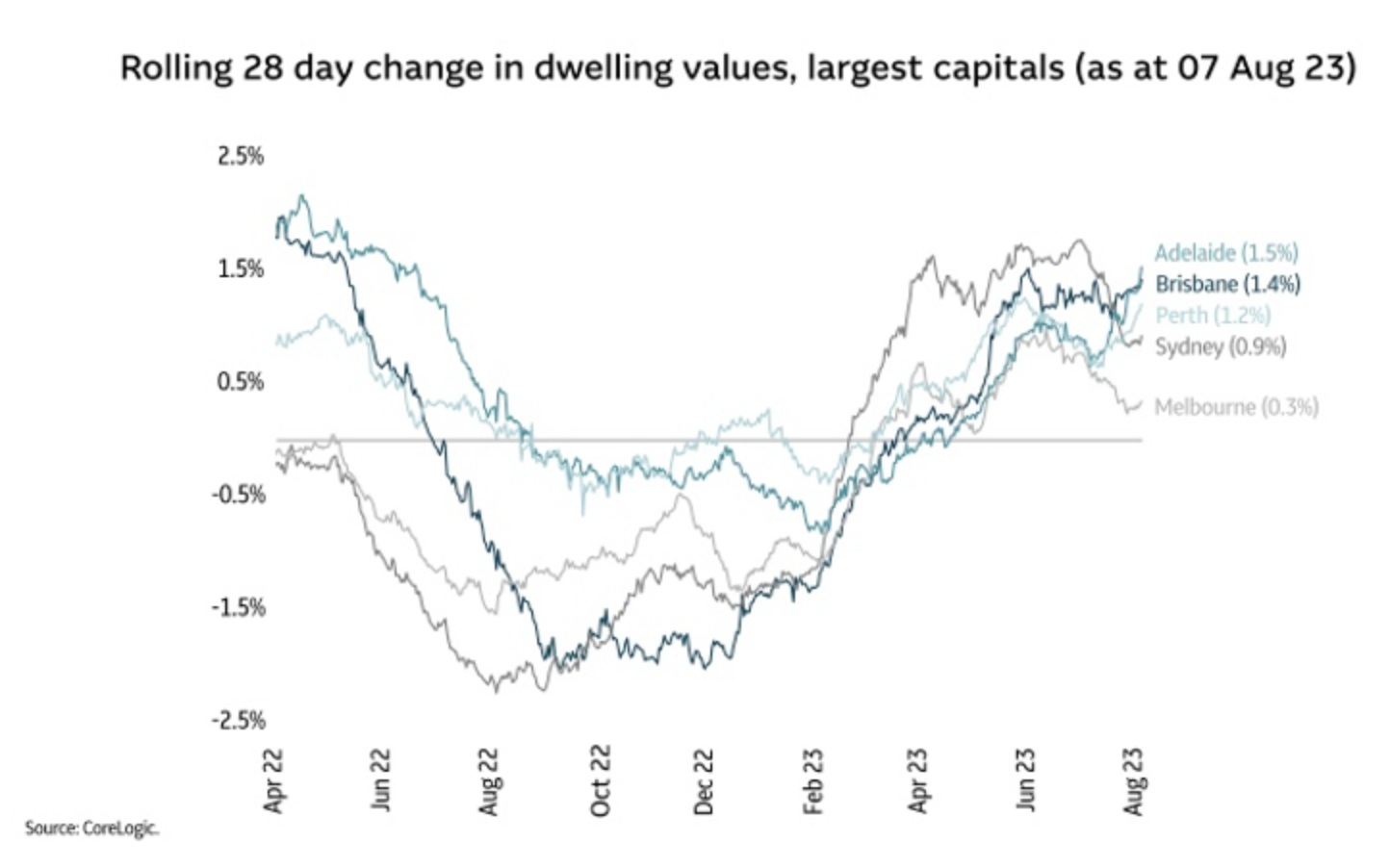

“Sydney and Melbourne appear to be leading this slowdown. These are two markets where housing is relatively unaffordable, but also where we have seen a visible lift in advertised supply,” Lawless observed.

Some regional markets, including the Gold Coast, Newcastle and the Illawarra, are still recording strong growth over the past three months. Gold Coast values rose 4% in that period.

“It’s going to be really interesting to see where those inflection points are as supply continues to come to market, and at what point will it outstrip the demand that still exists,” Thompson said.

2. Despite reaching the ‘fixed-rate cliff’, mortgage arrears remain in check

A significantly larger than average number of home loans were fixed between mid-2020 and mid-2022 – accounting for 46% of all secured housing finance at its peak in July and August 2021. The majority of these facilities are expected to expire this year, potentially putting additional stress on borrowers who may struggle to service their loans on higher interest rates.

Yet, as of March this year, 99.5% of borrowers remain on track with their mortgage repayments1, and arrears remain low.

“It looks like most borrowers are contending with rate rises so far. But this has been accompanied by a sharp drop in household savings, and consumers pulling back on discretionary spending,” said Thompson.

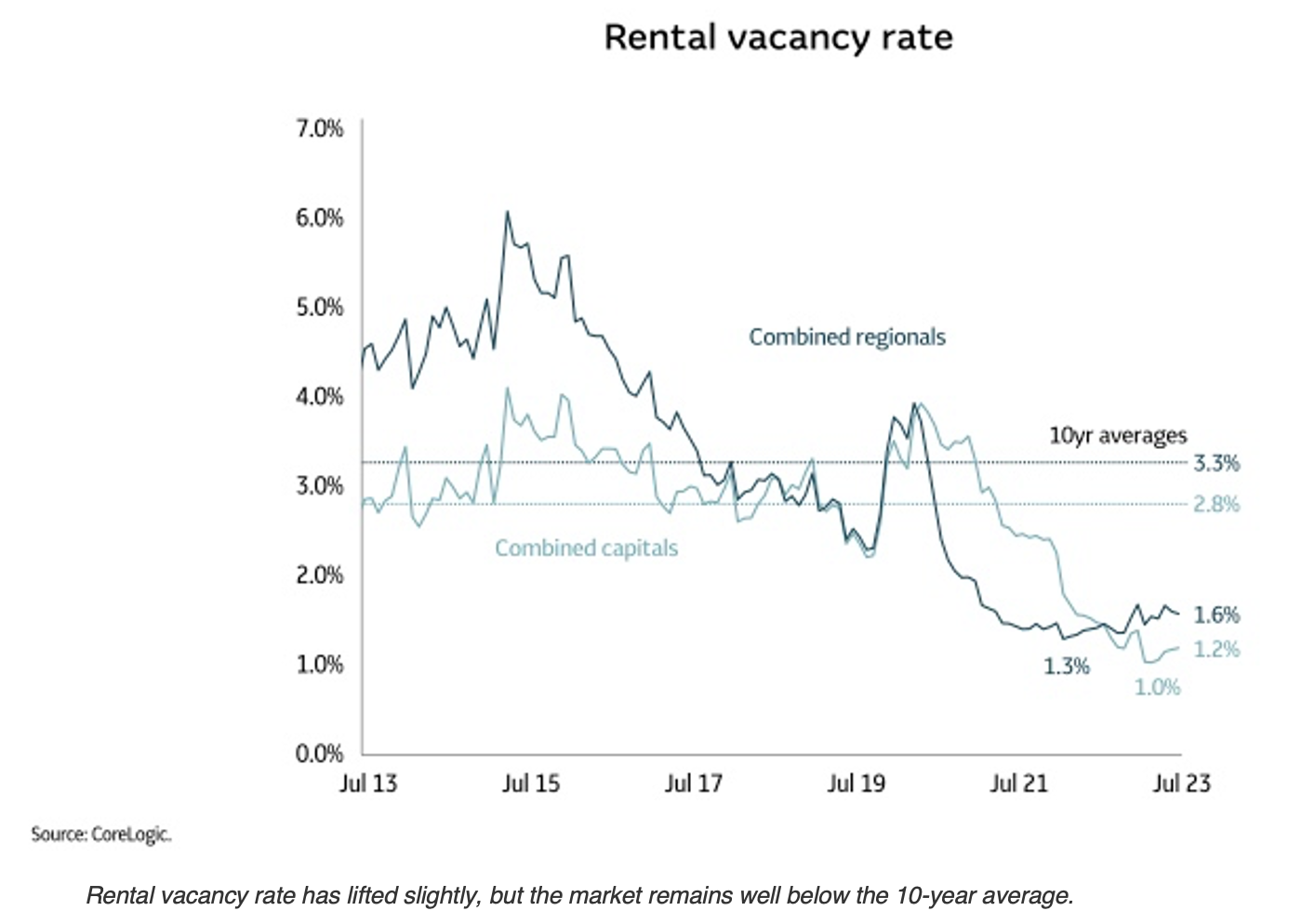

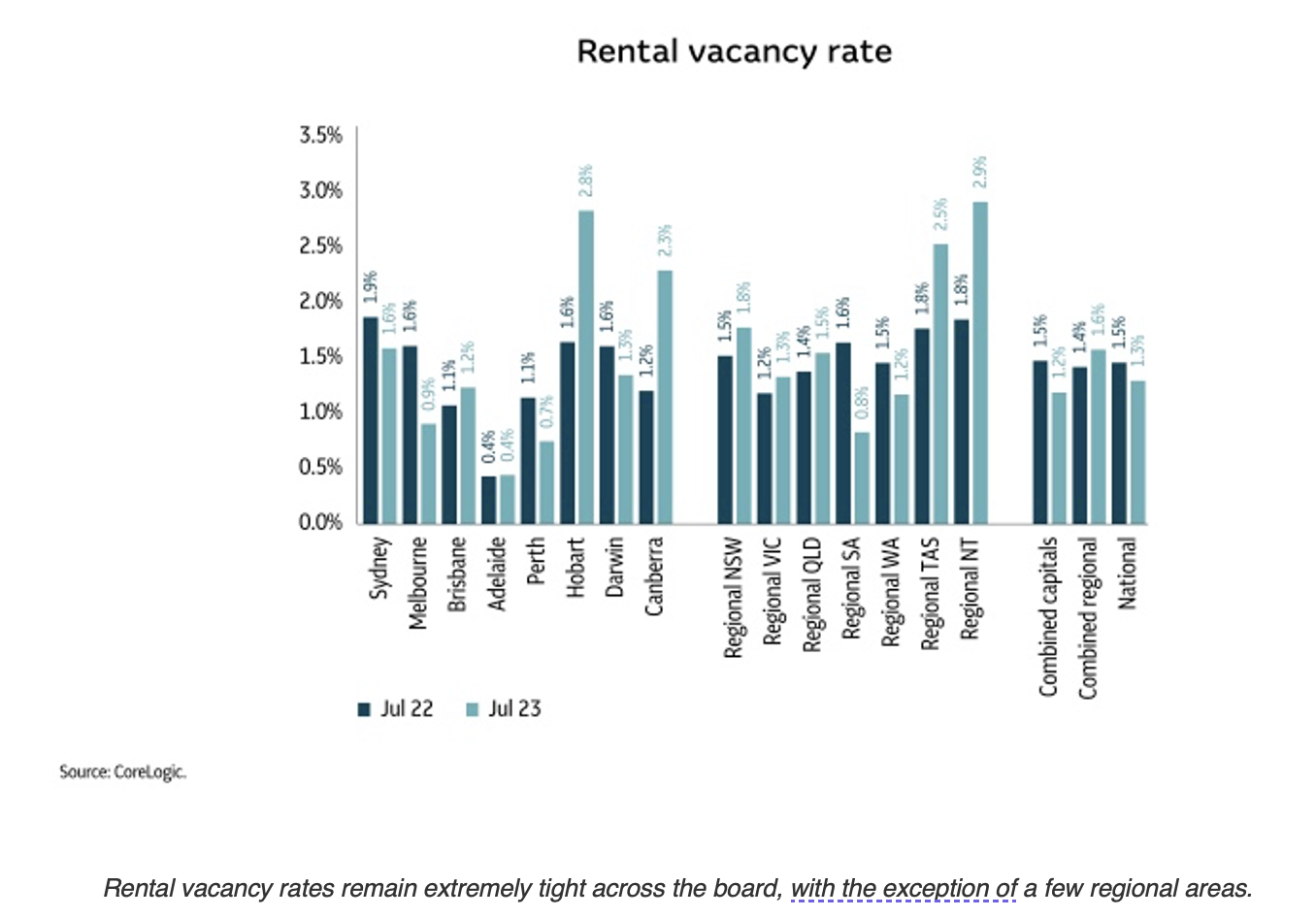

3. Rental market to remain tight

Rental vacancy rates have edged slightly higher from 1% to 1.2% across capital cities, and to 1.6% from 1.3% in regional areas. However, the rental market remains extraordinarily tight.

With no adequate supply on the horizon and net migration projected to reach 1.755 million between 2023 and 20282, vacancy rates are likely to remain low.

“Overseas migration creates an immediate demand for rentals, especially considering it is quite skewed towards students and short-term migrants rather than permanent migrants,” explained Lawless.

Although a tight rental market has pushed rental values up in more than 90% of Australian markets3 in the past year, recent growth has slowed slightly across the board.

“We’re starting to see a slowdown, even in the high-growth markets like inner Sydney and Melbourne. Part of that simply comes back to rental affordability pressures putting a ceiling on how high rents can eventually go,” Lawless shared.

In regional markets, migration back towards the capitals is also dampening growth.

“This is not necessarily because fewer people are moving to regions. It’s about more people moving from regional Australia to the capital cities.”

4. Despite strong rental conditions, more investors are selling

In July, investment properties accounted for around 37% of new listings in capital cities, compared to the pre-pandemic average of 23.6%. This surge in investor sales is likely due to holding costs outweighing rental gains.

“Servicing an investment loan has increased by at least $1,000-$1,200 a month in markets like Sydney, and a little bit less in some of the more affordable markets. Even though we’ve seen rents go up, the rise in rental income has only partially offset the increase in mortgage repayments in dollar terms. In Sydney, for example, monthly mortgage repayments might be about $1,200 higher, but rent has only gone up by $350 a month,” Lawless observed.

More leveraged investors who are feeling the pinch may also be concerned by debates around proposed policy changes, including land tax and rental caps.

“A lot of real estate businesses have seen significant decline in investor portfolios over a sustained period of time,” noted Thompson.

However, there are signs investment lending is starting to return. It accounted for the second biggest rise in lending activity since February.

“The return of investor appetite is being driven by tight rental markets, rising gross yields and more investors positioning for medium to long-term capital gains. We’re seeing some faith that markets have bottomed out, and hopefully interest rates have peaked as well,” said Thompson.

5. Development pipeline lacks approved supply

The trend in dwelling approvals across the medium to high-density sector has been below the 10-year average since 2018, and the sector will likely remain critically under supplied for the next five years4.

While a significant number of dwellings are under construction, approved supply in the pipeline is critically low.

“Even though we were moving through a peak in the number of homes that are under construction, a lot of this is related to the HomeBuilder grant. Because of supply chain constraints, bottlenecks and materials and labour shortages, completion of these developments has been prolonged,” Lawless pointed out.

New construction is expected to fall to 127,500 dwellings in 2024-20255 – down from 148,500 in 2022-2023.

Elevated costs and labour shortages remain major challenges for delivering supply in the future.

“The hard part for many builders and developers will be delivering stock to the marketplace with a profit margin. They may struggle to offset the rise in construction costs given consumers may not be able to tolerate significant price rises.”

And while construction costs are not likely to fall, developers can expect to make decisions with a little more certainty, as the growth of construction costs continues slowing down – rising 0.7% over the June quarter, below the pre-COVID decade average of 1.0%.

Looking ahead

So, what’s in store for the second half of the year?

“The key factor to watch moving forward is what happens with supply coming onto the market, especially as we move into the traditionally active spring season,” said Thompson.

If you have any concerns on your position or want specific advice to your circumstance, please contact us so that we can help you with your concerns and help to develop a solution that suits your requirements.

Contact the Client Care Team today.

See our other articles on our website relating to markets:

The Australian Residential Property Market

What to do when the next market correction happens and what not to do

Scary Markets, and you’re all familiar with our