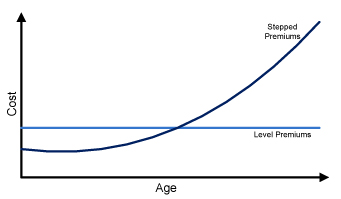

Insurance companies calculate their premiums by analysing the statistical data of the people who have made claims for insurance. This data has shown that as people get older, they tend to be more likely to make a claim. This means that as you get older, you become more risky to insure. As such, premiums increase to reflect the higher level of risk the insurer takes. These increases in stepped premiums will generally be exponential (as seen in the diagram below) until the insurance expires. However, several other factors will affect premiums and how much you pay for cover. These are discussed further below.

| What Affects Premiums? |

Several factors will affect the insurance premiums you pay. Below is a list of some of the most common factors Insurance premiums are usually available in two forms:

Amount of Cover

As expected, the more you are insured for, the greater your premiums will be. This is why it is important to ensure you have the right level of cover and review your needs when your financial circumstances change.

Stepped or Level Premiums

- Stepped Premiums – Insurance costs increase each year in accordance with your age; or

- Level Premiums – Insurance premiums are constant year to year, although most companies reserve the right to increase level premium rates, so it is not guaranteed that premiums will remain the same each year.

Stepped premiums are usually lower in the early years of insurance, but level premiums may be more cost-effective over the longer term.

We usually recommend a stepped premium structure as it allows you to obtain the required amount of insurance whilst minimising the impact on overall cash flow. Over time we generally review your level of cover to determine if it is sufficient and potentially reduce it as you build up more assets.

CPI Increases

Premiums can also increase at a faster rate with the inclusion of CPI indexation on the policy. This increases your level of insurance each year in line with national inflation. However, It is important to note too that despite the name, level premiums can rise too as the insurer reserves the right to do so.

Indemnity versus Agreed Value

Income protection policies may be issued as agreed value, guaranteed agreed value or indemnity. An agreed value policy means that the insured monthly benefit, plus any indexation increases, will be payable at the time of claim regardless of any reduction in the insured’s income since commencing the policy.

Guaranteed (or financial endorsed) agreed value contracts are those where sufficient financial information has been provided prior to the commencement of the policy to allow a claim for total disablement to be paid without further financial justification. Where this financial endorsement or guarantee does not apply, the financial justification for the insured benefit may be sought at the time of claim.

Indemnity policies provide a limit on the benefit payable, such that at the time of claim, the maximum benefit payable is a factor of the income the insured has earned (generally) in the 12 months leading up to claim. This means that if the insured has suffered a drop in income since taking out the policy, the benefit payable may be less than the insured monthly benefits. Indemnity policies usually cost less than agreed value policies and maybe a discount option on a standard policy.

Standard versus Comprehensive Cover

Standard cover only covers basic features such as the benefit are payable in the event of total disability, partial disability, rehabilitation and unemployment.

Comprehensive cover covers in addition to the basic cover, which includes accommodation, family support, home care and specific injuries benefits. Hence, the premium for a comprehensive cover is higher compared to the standard cover.

It should be noted that each insurer will have a list of optional benefits which can be added to the standard cover which are designed to provide greater benefit in the event of a claim. This provides the insured the ability to customize their cover and include extras they see as beneficial. Each of these extra cover options will increase the premiums paid.

Waiting Period

When considering an income protection policy, it is important to be aware of the waiting period involved before a claim can be made. In the event you are unable to work due to sickness or injury, there is a waiting period from the day you stop working before you can make a claim. The waiting periods on income protection usually range from 14 to 90 days. Generally, the shorter the waiting period, the higher the premiums will be.

Benefit Period

Similar to the waiting period, there is also different lengths of benefit period for income protection cover. These generally range from 2 to 5 years (up until the age of 65, at which time most policies will expire). Again, the longer the benefit period on the policy, the higher the premiums will be.

Underwriting

Underwriting is the process the insurance company takes to evaluate the risk they are taking by insuring you. Underwriting is specific to your health, lifestyle, occupation and extracurricular activities.

Each of the above categories has a scale from low risk through to high risk, which will have a direct effect on the premiums you pay. When it is deemed by the insurer that there is excess risk to insure you as an individual, they will generally charge a loading on your premium to account for these additional risks.

Some examples of things that could increase your premiums include being overweight, have prior medical conditions, being a smoker or heavy drinker, working in an occupation deemed higher risk or if you are involved in sports or hobbies that may increase your chance of injury, sickness or death.

Important information and disclaimer

This publication has been prepared by AustAsia Group, including AustAsia Financial Planning Pty Ltd (AFSL 229454).

Any advice in this publication is general only and has not been tailored to your circumstances. Accordingly, reliance should not be placed on the information contained in this document as the basis for making any financial investment, insurance, or other decision. Please seek personal advice before acting on this information.

Information in this publication is accurate as at the date of writing, 20 April 2020. Some of the information has been provided to us by third parties. While it is believed the information is accurate and reliable, the accuracy of that information is not guaranteed in any way.

Opinions constitute our judgement at the time of issue and are subject to change. Neither the Licensee nor any member of AustAsia Group, nor their employees or directors give any warranty of accuracy, nor accept any responsibility, for any errors or omissions in this document.

Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. It is not intended to be a substitute for specialised taxation advice or an assessment of your liabilities, obligations or claim entitlements that arise, or could arise, under taxation law, and we recommend you consult with a registered tax agent.